Intesa: Questions On Dividend Sustainability.

Riportiamo integralmente questo interessante post odierno di zerohedge.com

Intesa Sanpaolo: Questions On Dividend Sustainability Weigh Heavily

Intesa stands out from its peers for its cost efficiency, strong credit quality and robust capital position. Amongst European banks it is clearly a quality play.

But the story has become dominated by the dividend and many investors seem increasingly to question whether it is prudent for the company to stick to an 80% payout target.

1Q results were better than expected and management remains very confident on the profit outlook for the full year.

But the revenue environment is tough, which makes the dividend more reliant on further cost cuts or loan loss reductions, both already at low levels.

With Intesa having become such a single issue stock, the risk is that any disappointment on the dividend will prompt a brutal share price reaction.

Thesis: Intesa (OTCPK:IITOF) yields 8% and has become a favourite amongst income investors in European banks. However, maintaining such a high payout ratio in an environment where capital regulations are uncertain and the profit outlook is weak seems a risky strategy. With the dividend having become such a defining issue and with the stock trading at a premium valuation to peers, the downside risks to the share price are large if expectations cannot be met.

A quality name in a sector that has too few of them

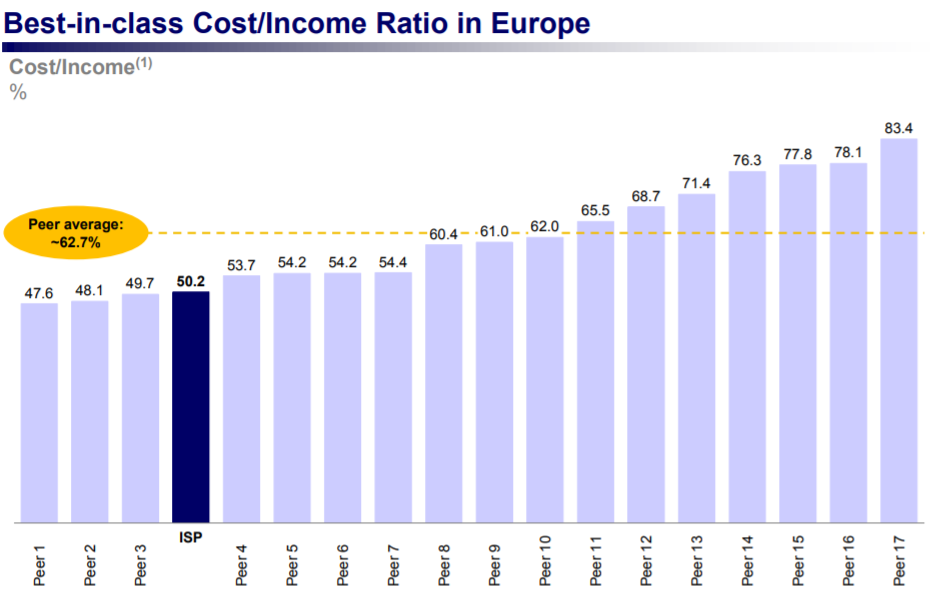

At close to 0.9x net asset value and 10x estimated 2019 earnings, Intesa trades at a premium to many of its European banking peers. This reflects its status as a quality name in a sector with all too few of them. In particular, the company’s ability to control costs has been a substantial benefit in what has been an exceptionally challenging revenue environment for the industry in recent years. Cost:income is currently 50%, a level only three other banks in Europe have achieved.

Intesa is a European banking cost leader

Source: 1Q19 results presentation

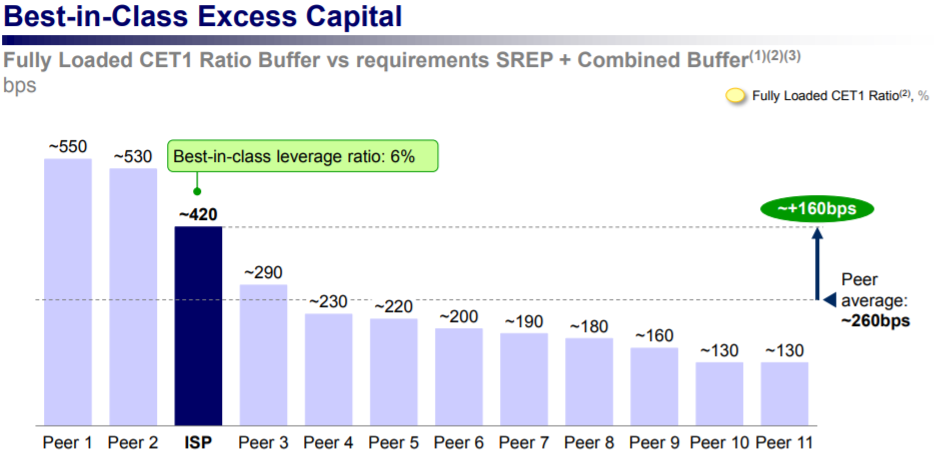

In addition, the company has maintained a solid balance sheet despite all the challenges of operating in recessionary Italy. Non-performing loans have fallen to 4.1% of the loan book, their lowest level since 2008 and the nominal value of the non-performing portfolio is only half the level it was in 2015. This has been achieved while maintaining a regulatory capital ratio (13.5%) that is 420bps above Intesa’s minimum requirement. Only two other banks in Europe have a higher capital buffer above regulatory required levels.

Intesa also has amongst the most solid capital positions of its peers

Source: 1Q19 results presentation

But the dividend has come to overshadow all else

The problem I see for Intesa is that the market has stopped rewarding these factors. In part this is because other banks have got better: The dispersion between the best and worst performers in Europe on metrics like capital and loan portfolio quality has narrowed significantly over the last few years as GFC-era restructurings have run their course.

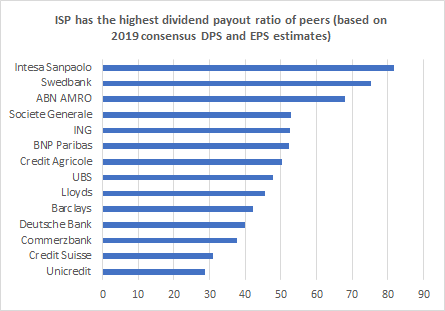

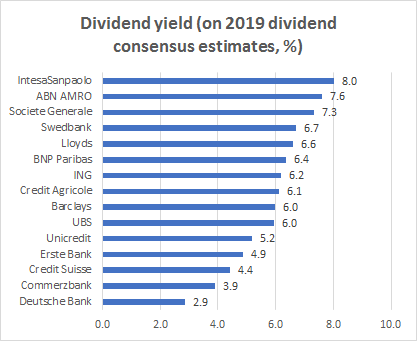

It also reflects that, in the case of Intesa, the market’s focus has come to be dominated almost exclusively by the dividend and its sustainability. Intesa currently has a dividend payout ratio target of 80%, which puts it way above almost all other banks in the sector (the sector average payout ratio is 50%). It is an easy target for investors to criticise since most other banks in Europe are still mainly focused on retaining rather than distributing capital given the uncertainties in the regulatory environment. Indeed scrip dividends are still a feature for several major competitors e.g. Societe Generale (NYSE: SCGLF) and Santander (NYSE: SAN).

Source: Thomson Reuters consensus data

In this context, Intesa’s recommitment to such a high payout level sets it apart and also leaves it open to the charge of being imprudent.

1Q results were better than expected but also highlighted the risks

1Q surpassed Street expectations with net profit reported at €1.05bn against a consensus estimate of €0.9bn. But the results also highlighted where the risks to the dividend reside.

The revenue environment is clearly weak, as it is for many banks, and management cited aggressive competition in Italy in the lending market as well as the negative impact on retail investment activity from volatile markets. 1Q revenues fell 3.5% year over year.

To maintain the current profit level, the company is therefore increasingly dependent on cutting costs and cutting loan losses.

The 1Q cost performance was admittedly impressive. Costs were down 4.5% year over year and amongst the biggest annual reduction reported by any bank in Europe this quarter.

The same is true of loan losses where inflows into the non-performing loan portfolio being at a record low and the overall stock of non-performing loans fell another 3% compared to the end-2018 level. Provisioning for loan losses through the P&L fell by 24% year over year.

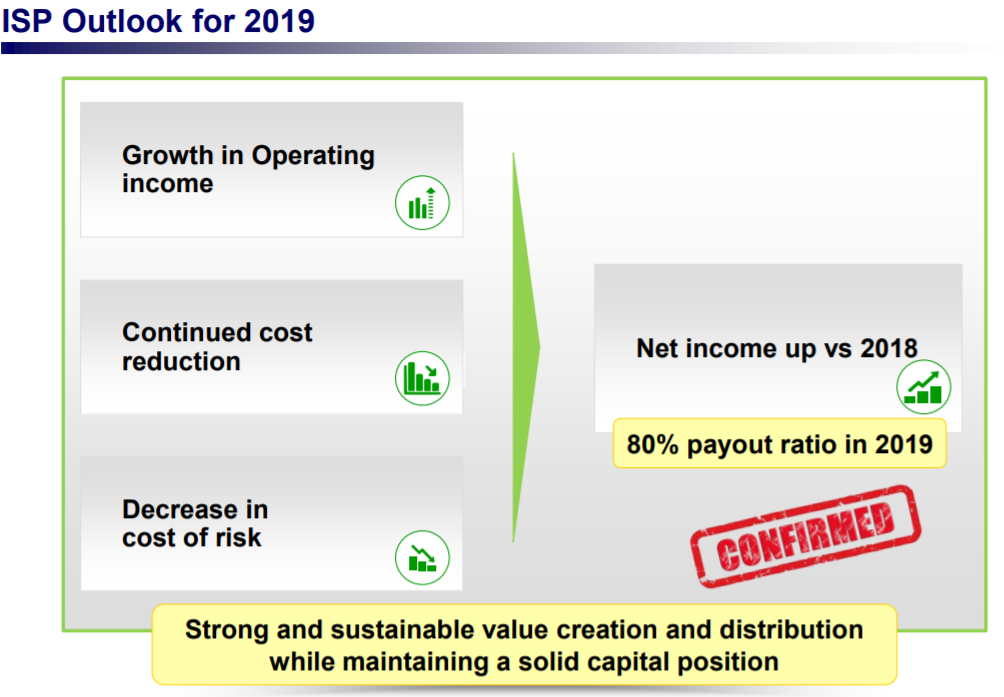

Management also reconfirmed key guidance metrics for 2019, including higher year-on-year revenues, higher net profit (by implication above €4bn) and the 80% dividend payout target.

Management is confident of meeting 2019 targets

Source: 1Q19 results presentation

The catch is that with costs and loan loss provisioning now being at such low levels, it is increasingly hard to see either line item remaining a driver of profit growth in the future if revenues continue to fall.

But any slip-ups will put intense focus on the sustainability of the dividend

This shifts the focus back to the main issue: the sustainability of the dividend. The market is clearly already nervous. Consider, for example, Street estimates for the dividend level in 2019. Management’s guidance is for net profits of >€4bn. The 80% payout target should imply a dividend of at least €0.22 yet consensus for 2019 is only €0.18.

Indeed at €0.18, the market clearly already fears a cut since Intesa has just declared €0.197 for 2018.

The yield in itself is a red flag in my view being well above the level of peers. Not many companies manage to maintain yields above 8%: eventually, either the market is proved correct and the dividend is cut or the share rises to bring the yield down to peer levels. In this case, I fear the outcome is likely to be the former.

Source: Thomson Reuters consensus data

Conclusions

Management is caught in a guessing game with the market around the dividend where they are determined to continue the growth path of recent years while many investors clearly believe a cut is on the cards as revenues disappoint and tougher regulatory capital requirements start to bite.

The outcome won’t become clear probably until we get closer to the full year 2019 results and this holds the prospect of several quarters of uncertainty and volatility in dividend estimates. I see this holding the share back given it already trades at a premium to peers and given the importance of the dividend yield to the broader investment case for Intesa.

I’d be looking at other cheaper alternatives in the sector where attractive yields are protected by better earnings coverage than Intesa currently offers.

Stocks mentioned and tickers:

| DB | Deutsche Bank |

| OTCPK:UNCFF | UniCredit |

| OTCPK:CRZBF | Commerzbank |

| CS | Credit Suisse |

| BCS | Barclays |

| UBS | UBS |

| ING | ING |

| LYG | Lloyds Banking Group |

| OTCQX:BNPQF | BNP Paribas |

| OTCPK:ABNRY | ABN AMRO |

| OTCPK:SWDBF | Swedbank |

| OTCPK:SCGLF | Societe Generale |